The law behind it

The right comes from the Late Payment of Commercial Debts (Interest) Act 1998. It gives a business that’s owed money a statutory right to claim interest and a fixed compensation sum from a late-paying business customer.

It applies to business-to-business transactions and to public sector customers. It does not apply where your customer is a private individual buying as a consumer.

When an invoice legally becomes late

If you agreed a payment due date, the invoice is late the day after that due date passes (usually within 30 or 60 days).

If you didn’t agree a date, the law treats payment as late 30 days after the later of two points:

- The day the customer received the invoice, or

- The day you delivered the goods or service (if this is later).

This is part of the law and a non-negotiable of applying late payment fees.

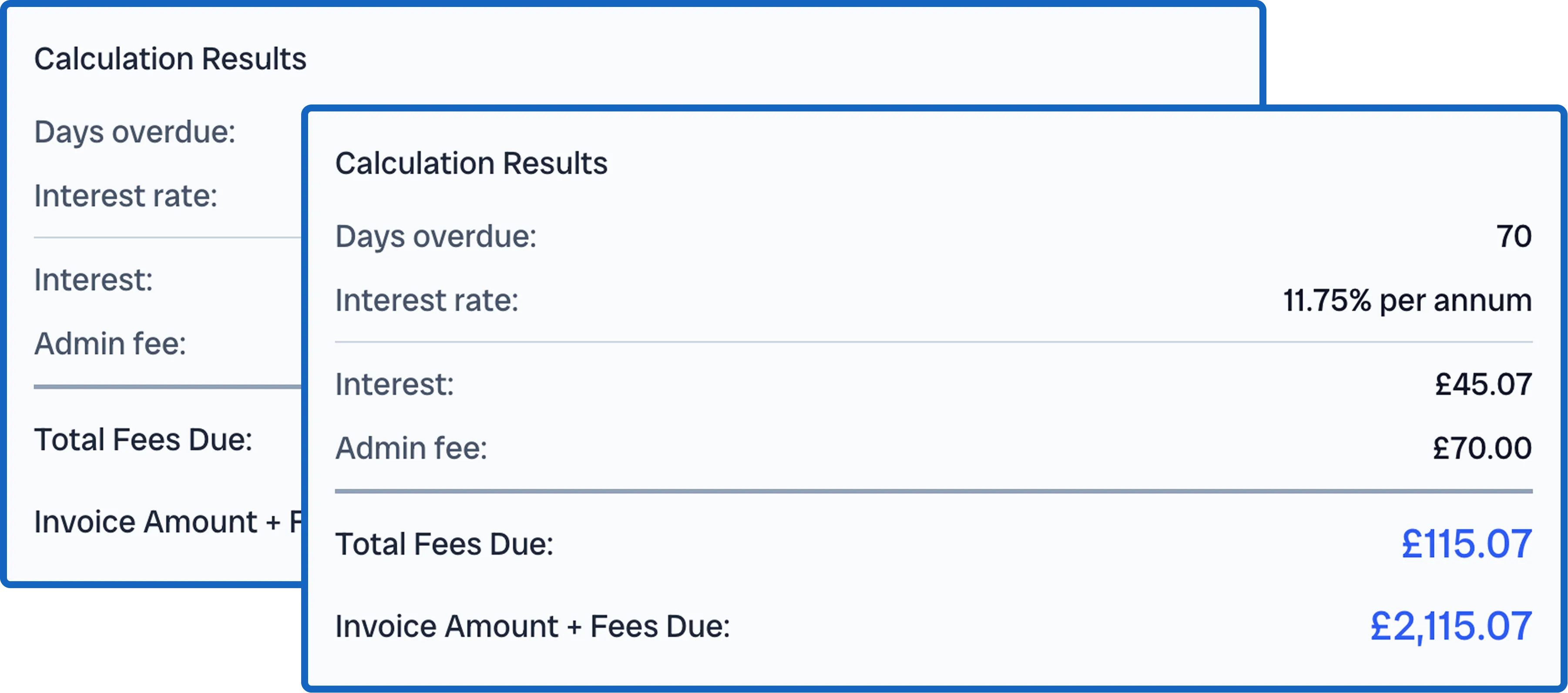

Interest rates for late payment fees

Statutory interest is 8% above the Bank of England base rate. The detail that trips people up is which base rate to use.

The rate is fixed for six-month reference periods:

- For debts that become late between 1 January and 30 June, use the base rate from the previous 31 December

- For debts that become late between 1 July and 31 December, you use the rate in force on the previous 30 June

That reference rate then applies for the whole period, even if the Bank of England changes its base rate in the meantime.

This approach to fixing rates was part of the 2002 update to the 1998 Late Payment Act and is explained in government documentation here.

Any errors to calculating UK interest can be avoided by using an automated tool (like Trove’s free one).

How much compensation you can claim

On top of interest, you can claim a fixed compensation sum per overdue invoice:

| Invoice amount | Compensation fee |

|---|---|

| Up to £999.99 | £40 |

| £1,000 to £9,999.99 | £70 |

| £10,000 or more | £100 |

If your reasonable costs of recovering the debt are higher than the fixed sum - for example debt collection or legal fees - you can claim the difference on top, provided the costs are reasonable and you can evidence them.

Do you need it in your contract?

No. The statutory right applies whether or not it’s in your terms. But including a clause is best practice, because it sets expectations up front and gives you something clear to point to if a customer disputes the charge. Here’s a sample paragraph:

Contract clause

If any invoice is not paid by the due date, we reserve the right to charge interest on the overdue amount at the statutory rate of 8% per annum above the Bank of England base rate, in accordance with the Late Payment of Commercial Debts (Interest) Act 1998. We may also charge a fixed compensation fee for debt recovery costs as set out in the Act. Interest will accrue daily from the date payment becomes overdue until the date of actual payment.

Charging consumers is different

If your customer is a private individual rather than a business, the 1998 Act doesn’t apply. You can still charge a late fee, but only if it’s set out in your contract, and it has to be a reasonable reflection of your costs rather than a penalty. The flat statutory amounts above don’t apply to consumer invoices.

This is general information, not legal advice. For a specific situation, check with a qualified solicitor.

Automatic late fees - launching July 2026

Trove is launching a late payment fee plan, free for all Xero users. Join the waitlist to be notified when it goes live and get early access.