Two routes through this guide. If you run a finance team, or you're buying for a mid-market or enterprise business, the tools, pricing and trade-offs that matter to you are in our credit control software compared guide. If you're a small business or startup - usually on Xero, often with the owner still doing the chasing - start with credit control software for UK small businesses. This page is the map of the whole market; those two are the routes through it.

Credit control software automates the work of chasing unpaid invoices: tracking who owes what, sending overdue invoice reminders, doing it all automatically. It’s also sold as accounts receivable (AR) automation, debtor management, or collections software, which all describe overlapping versions of the same job. Most small businesses using Xero already handle invoicing and payments, so the only piece they’re missing is collections - getting paid. This guide explains what these tools do, how they differ, what they cost, and how to choose the right one for a UK small business.

What is credit control software and do most small businesses actually need it?

Credit control software is the layer that chases your unpaid invoices for you. Instead of you remembering who’s overdue and writing the same awkward email for the fifth time, it sends reminders on a schedule, keeps a record of every chase, and escalates when customers don’t respond.

It helps to see where it sits in the bigger picture. Getting paid has three stages: you send the invoice, most customers pay and you chase anything that’s late. Accounts receivable is the umbrella term for all three. Credit control and debtor management cover the last stage only - the chasing.

That distinction matters when you’re choosing a tool. If you use Xero, you usually have invoicing and payments handled. You raise invoices in Xero and customers pay by bank transfer or a Stripe or GoCardless payment link. The stage that’s still manual is the chasing and that’s the only stage most Xero users need to fix.

In a nutshell: if you already send invoices, the majority get paid and your problem is those final few late payers, you need credit control software. That’s what this guide focuses on.

Credit control, debtor management, dunning: what’s the difference?

These terms get used interchangeably and which one you use mainly depends on which geography you’re in. While accounts receivable covers the full invoice to cash process, these three terms focus on cash collection. Here’s an overview of the differences:

| Term | What it covers | Where it’s used |

|---|---|---|

| Accounts receivable (AR) | The whole process: raising invoices, taking payment, and chasing what’s late | The umbrella term, used in all geographies |

| Credit control | Chasing, getting paid, credit risks and limits | Mainly UK |

| Debtor management | Effectively the same as credit control | Mainly Australia and New Zealand |

| Dunning | Chasing, getting paid; less of the credit risk management | Mainly US |

Credit control and debtor management describe the same job in practice, so don’t read too much into which one a tool uses. FreeAgent (UK based) calls this category of apps “Credit Control”, Xero (New Zealand based) calls it Debtor management.

FreeAgent labels this section “Credit Control”

Xero labels the same functionality “Debtor Management”

“Dunning” is slightly more limited to the automated system and generally does not include credit risk management. It’s more common in the US and in software documentation than in everyday UK use.

Some tools span the whole umbrella. Chaser, for example, markets itself as both accounts receivable and credit control software. That isn’t a contradiction - accounts receivable is the wider category, so a tool can sit across all three stages and still do credit control as part of it.

The takeaway: for a UK small business, credit control, debtor management, and dunning all point to roughly the same thing - a tool that helps you collect unpaid invoices. Accounts receivable is the bigger box that also includes the parts you’ve probably already sorted.

What features sit in the collections layer?

Once you’ve narrowed it down to credit control rather than a full AR platform, the next question is which features actually matter. They split into the ones you’ll want from day one and the ones that only start to earn their keep as you grow.

Must-have features

- Xero sync. Two-way sync from Xero to your credit control software and back again.

- Automated invoice chasing. The core job.

- Send via your domain. Reminders sent from your email address, with your branding.

- Notes and tasks. Somewhere to log everything that’s not an email.

- Basic reporting. A clear view of what’s overdue, outstanding and paid.

Nice to have (more relevant as you grow)

- Advanced reporting. Technical analysis with metrics like DSO, AR ageing, CEI.

- Slack / MS Teams integration. Alerts pushed into the channels your team uses.

- CRM integrations. Linking payment activity to your customer records.

- Credit limits / risk scoring. Managing credit risk for each customer.

- Late fee automation. Calculate and apply UK late fees and statutory interest.

Which integrations matter most depends on the rest of your stack. If you run credit checks, see how tools connect to CreditSafe. If your team is on Microsoft 365, see which tools integrate with Xero, Outlook and Microsoft Teams. If you’re on Google Workspace, see which connect Xero, Gmail and Slack.

The market: where each tool focuses

The tools in this space fall into two rough groups, depending on how much of the invoice-to-cash process they cover. The line isn’t rigid - some tools straddle it - but it’s a useful way to see the landscape.

Full-cycle, accounts-receivable-leaning. These do more than chasing - invoicing, payment collection, and sometimes credit risk all in one platform.

- Chaser - chasing-first but spans the full AR cycle, popular with UK mid-market finance teams

- Upflow - AR platform aimed at B2B SaaS and scaling companies, strong on payment and reporting

- Kolleno - AR automation covering collections, payments and reconciliation

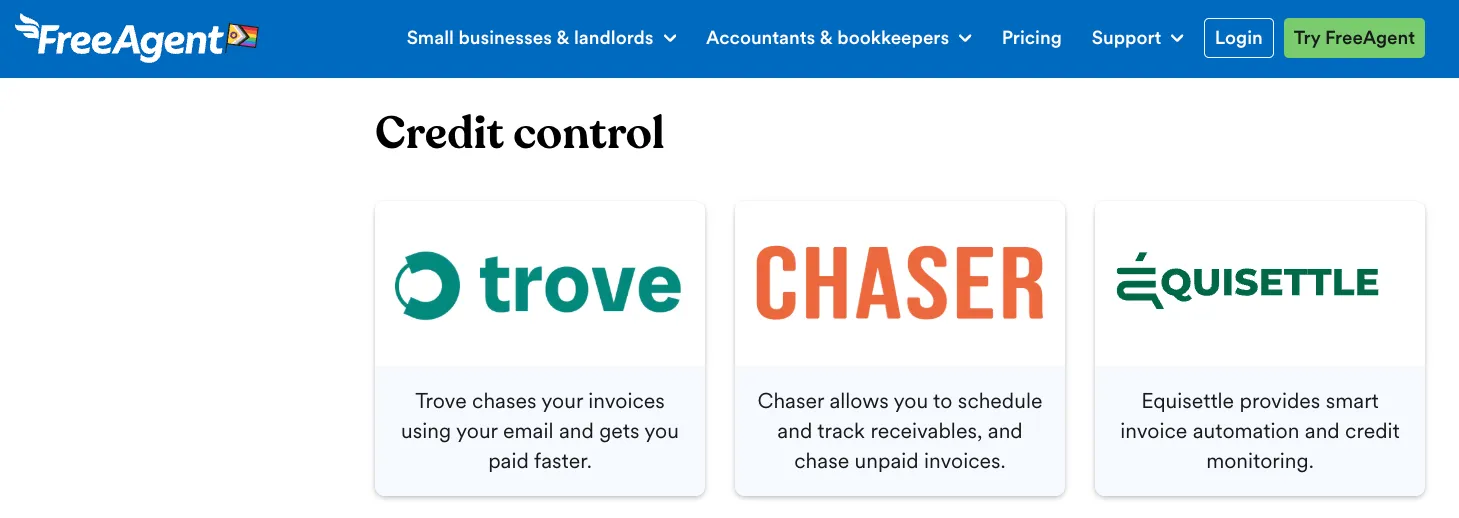

Collections-focused. These focus on one job - chase unpaid invoices - and tend to be simpler and cheaper.

- Trove - invoice chasing with CRM integrations and late fee automation

- Satago - credit control with credit risk and financing options layered on

- Paraglide - AI-led chasing and inbox management

- Lunos.ai - AI-led chasing and dispute management

The free baseline. Xero’s built-in invoice reminders. Free, fine for the simplest needs, and the thing every other tool is effectively competing against. We’ll come back to where they run out of road.

For the deeper market reviews, see our guides to credit control software for UK small businesses, AI credit control software for small businesses, and the best invoice chasing software for Xero users.

How much does credit control software cost?

Here’s how pricing compares across the main options. Two quick points:

- All prices are entry pricing - most tools charge more as your invoice volume grows.

- ‘Focused on’ is based on how each software talks about its users and the customers they highlight on the website.

| Tool | Focused on | Starting price | Pricing model | Free trial | Late fee automation |

|---|---|---|---|---|---|

| Satago | UK small business on Sage | £45/mo | Fixed | Yes | Yes |

| Trove | UK small business on Xero | £50/mo | Fixed | Yes - 30 days | Yes |

| Lunos.ai | B2B AR teams | 0.3% on collected revenue | $200 + 0.3% on collected revenue | Yes (until it collects an invoice) | No mention |

| Paraglide | High-volume B2B teams | On request | Not published | No mention | No mention |

| Chaser | UK mid-market finance teams | £199/mo | Fixed | Yes - 10 days | Yes |

| Kolleno | Mid-market and enterprise collections teams | £650/mo | Per user | No mention | No mention |

| Upflow | US B2B SaaS / scaling | On request | Not published | No mention | Yes |

Features and prices checked June 2026, based on each vendor's published pricing pages. Several tools (Upflow and Paraglide) don't publish standard pricing and quote on request. To read more on pricing, see our breakdowns of affordable dunning software pricing, Chaser and Upflow pricing compared, Kolleno and Upflow pricing compared, and the three-way pricing comparison of Chaser, Kolleno and Upflow.

The tools compared: short profiles

A closer look at each option, in the same format so you can scan across them.

Xero reminders (the free baseline)

- Xero rating: n/a (built in)

- Starting price: Free, included with Xero

- Target customer: Any Xero user with simple, low-volume chasing

- Best at working with: Xero (it is Xero)

- Integrations: None needed

- Standout feature: It’s free and already in your account

Xero’s reminders are a fine place to start. They’re free, they take about ten minutes to set up, and for a business with a handful of reliable customers they may be all you need. The limits show up as you grow: Xero caps you at five reminders per invoice, uses one schedule for every customer, sends from an @xero.com address that can get spam-filtered, emails all contacts rather than the right one, and can’t apply late payment fees. When those start to cost you, it’s time to look at a dedicated tool. There’s a full rundown of the limitations here.

Satago

- Xero rating: 4.9/5

- Starting price: £45/mo - next tier £80/mo

- Target customer: UK small businesses on Sage who want reminders plus credit checking and invoice finance in one place

- Integrations: Sage, Kashflow, FreeAgent, Quickbooks, Xero, Experian credit data, email

- Standout feature: Experian-backed credit risk scoring

Satago is a three-in-one product which gives you credit risk scoring alongside chasing. Worth noting for the Satago Basic plan: reminders send from Satago’s own email address rather than yours, which affects deliverability and professionalism. Sending from your own domain requires the £80 Premium plan.

Trove

- Xero rating: 5/5 (Xero 2026 Growth App)

- Starting price: £50/mo - next tier £135

- Target customer: UK small businesses on Xero who want to automate invoice chasing

- Integrations: Xero, FreeAgent, Stripe, email (Gmail, Outlook), Slack, MS Teams, Hubspot, Copper, Hyperline

- Standout feature: AI that keeps emails sounding human and manages chasing admin

Trove is Xero-native, designed for the gap between sending an invoice and getting paid. It runs per-customer reminder sequences, sends from your own email so messages don’t get spam-filtered, and can calculate and raise UK late payment fees automatically.

Lunos.ai

- Xero rating: Not listed in app store

- Starting price: 0.3% on collected revenue

- Target customer: B2B AR teams

- Integrations: Broad - billing, CRM, ERP, support tools

- Standout feature: AI that handles dispute management

Lunos gives your AR team back-up when handling dispute management. It helps gather the relevant information and then present it back to the client to move the dispute along.

Paraglide

- Xero rating: Not listed in app store

- Starting price: On request (not published)

- Target customer: High-volume B2B teams

- Integrations: Broad - billing, CRM, ERP, support tools

- Standout feature: Agentic AI that handles billing queries inside the finance inbox

Paraglide sits more on the AR-platform side than the simple collections side, and is aimed at bigger, more operationally complex teams. It promises to get you to inbox zero on your finance inbox.

Chaser

- Xero rating: 5/5

- Starting price: £199/mo - next tier £599

- Target customer: UK mid-market finance teams

- Integrations: Broad - billing, CRM, ERP, support tools

- Standout feature: Built-in pathway to debt collection, also by Chaser

Chaser is one of the most established names in the space and spans the full accounts receivable cycle. It suits a finance team that wants detailed control over chasing workflows and reporting. For the head-to-head, see Chaser vs Upflow and our list of the best Chaser alternatives in 2026.

Kolleno

- Xero rating: 5/5

- Starting price: £650/user/mo - next tier £1245

- Target customer: Mid-market and enterprise collections teams

- Integrations: Sage, Quickbooks, Xero, plus ERPs, CRMs and 1,000+ via its platform

- Standout feature: E-invoicing as part of the full AR workflow

Kolleno is an enterprise-level platform which covers the full AR lifecycle from invoicing to collections. They have recently launched AI agents which could be similar to the functionality provided by Lunos and Paraglide. Compared directly with Upflow here.

Upflow

- Xero rating: 5/5

- Starting price: Not published; historically billed as a percentage of revenue collected

- Target customer: B2B SaaS and scaling companies, often US-based

- Integrations: NetSuite, QuickBooks, Xero, Stripe, Zuora, Salesforce, plus API

- Standout feature: Sophisticated AR analytics - DSO tracking, cohort analysis, risk scoring

Upflow leans towards larger, faster-growing B2B companies, often US-based, with the reporting depth and integrations that suit a dedicated finance function. It has deep AR reporting functionality that is a genuine differentiator for bigger AR teams. Compared directly with Chaser here and compared directly with Kolleno here. For an all-three round-up covering Chaser, Kolleno and Upflow together, see our credit control software compared.

How do I choose software for chasing unpaid invoices?

Work through it in three steps: features, budget, role.

1. Do you need the nice-to-haves?

Advanced AR reporting, Slack or Teams alerts, CRM integrations, and credit limits or risk scoring all matter more as you grow, and you generally pay more to get them.

So the real question is whether you need them yet. For most small businesses the honest answer is not yet - and paying for a heavier platform to get features you won’t use is the most common way to over-buy here.

2. What’s your budget?

- Lower price. Tools that do the core job well without the extra weight. Satago, Trove and Lunos sit here. This is where most UK small businesses on Xero should be looking.

- Higher price. Fuller platforms like Chaser and Kolleno worth it when you have a finance team that will use the extra reporting and workflow control.

3. Who’s doing the chasing?

Within a bucket, the right tool often comes down to who runs it day to day:

- A director or owner doing it themselves wants something simple that mostly runs itself - lean to the collections-focused, lower-price end.

- A bigger finance team wants control, customisation and reporting - the fuller platforms earn their cost.

- A dedicated credit controller wants workflow depth and account-level detail - the higher-feature tools suit best.

These are the three best questions to start with when making the decision.

Frequently asked questions

Is credit control software worth it for a small business? If late payments are costing you time or cash flow, usually yes. The maths is simple: if a tool costing a modest monthly fee gets invoices paid days or weeks sooner, it pays for itself quickly. If you only have a few reliable customers and rarely chase anyone, Xero’s free reminders may be enough.

What’s the difference between credit control and debt collection? Credit control is the ongoing process of chasing invoices so they get paid on time, done by you or a tool on your behalf. Debt collection is what happens when that fails - handing an unpaid debt to a third-party agency or solicitor to recover, usually for a fee or a cut of what’s collected. Good credit control reduces how often you need debt collection.

Does credit control software work with Xero? Most do, through a two-way sync that pulls in your invoices and payment status and pushes back updates. If you use Xero, Xero integration should be a must-have - rule out anything that doesn’t offer it.

Can it charge late payment fees automatically? Some tools can. UK businesses have a statutory right to charge interest and a fixed fee on overdue B2B invoices, but Xero won’t calculate or raise these for you. Tools with late fee automation work out what’s owed and raise it as a separate invoice. See our guide to UK late payment fees.

Do I need this if I already use Xero’s reminders? Not always. Xero’s reminders are free and fine for simple needs. You outgrow them when you hit the five-reminder cap, need different schedules per customer, find reminders going to spam or the wrong contact, or want to charge late fees. At that point a dedicated tool earns its place.

Trove handles the collections layer for UK small businesses on Xero: per-customer reminders sent from your own email, and automated UK late payment fees raised straight into your account. It runs a free 30-day trial and connects to Xero in about five minutes. Start a free trial or book a demo if you’d like to see it first.